{kind=link}

Annuities are negotiable financial instruments that guarantee a steady income to their holder over a certain period of time. The annuity contracts are sold as products by different financial institutions like insurance company etc. Annuity investments are made as one-off payments or instalments with a view to receiving a fixed payout in a certain interval. Annuity products are mainly bought to secure a fixed income stream during retirement.

The Secondary Market Annuity

A secondary market annuity (SMA) is also the ordinary annuity the only difference is that the secondary market annuity (SMA) holders are willing to sell their annuity in order to receive cash now instead of future. SMAs are sold at a discount to compensate the buyers for paying cash now and receiving payout later. The term secondary market annuity also includes structured settlements and lottery payments. The buyer of the secondary marketing annuity is often the factoring companies who offer immediate lump-sum payment in exchange for a discount. Although selling a secondary market annuity requires court approval. You shouldn’t have any problem getting court approval if you have a proper reason to sell the annuity.

Selling Options

When it comes to selling annuity payments, the annuity holder has a number of options like selling the entire annuity, a number of payouts or, a lump-sum amount. It’s always a good practice to consult a lawyer or, financial advisor before choosing the option. Many countries or provinces require the owner to have a legal advisor.

1. Selling the Entire Annuity

Selling the annuity in its entirety remains the most popular option in the secondary market. This basically means you sell your whole contract and rights to any future payment. Therefore, you are no longer entitled to receive any future payout from your annuity. The annuity holder receives a lump-sum amount to meet his/her urgent financial needs whereas the buyer which is often the factoring company receives the advantage to buy the annuity at a discounted price and make a profit out of the transaction.

2. Selling A Number of Payouts

The annuitant can sell a specific number of payouts to the buyer. If an annuity holder needs some cash immediately to meet some urgent financial needs but doesn’t need the entire annuity amount now. In this case, he may choose this option. For example, if the annuity is supposed to make a yearly payout over the next 20 years and the annuitant needs money equal to 5 payouts, he may sell 5 years payment at a discount. In this case, his payout will stop for 5 years and resume after five years. He will keep receiving the payment for the next 15 years as per the agreement.

3. Selling a Lump Sum Amount

The annuity holder can also sell a portion of his/her future payouts in exchange for receiving a specific amount of money now. This is slightly different from the concept of selling a specific number of payouts. The major difference is that the transaction is based upon a specific amount rather than a number of future payouts. The owner stops receiving annuity payments until the specified amount is repaid to the buyer. After the repayment, the annuitant resume receiving the annuity payouts as usual.

The Annuity Selling Process

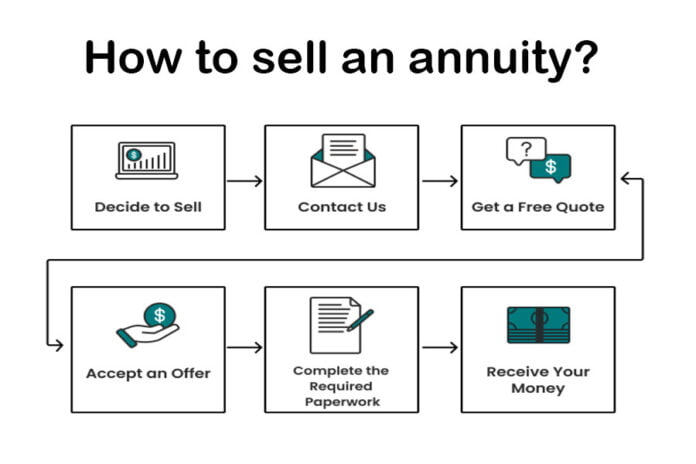

Selling an annuity is pretty straightforward in most cases. But in some situations, you may have to go through some extra administrations. Here is a list of processes an annuity holder needs to follow in order to sell his/her annuity on a secondary market.

Step 1 – Determine Your Financial Needs

At the very first stage, you need to determine your financial needs in order to decide whether you are selling your entire annuity or part of it. If you are to sell your annuity partially, then how much?

Step 2 – Do Your Homework and Research Buyers

You should always start by doing some ground research. All information is readily available online these days. A simple google search can help you find reputable buyers, their contact details, customer feedback etc. You can also consult a good financial advisor or an attorney specializing in this field as they can give you deep insight tailored to your situations.

Step 3 – Get a Free Quotes

After choosing the best buyers, start contacting them and asking for free quotes. You can normally request your free quotes via their websites. The company representatives will call you to discuss further regarding their offer. Once you have received a number of offers, compare and contrast them to figure out the option that serves your interest the best. Normally, you should prefer one easy to understand and the company is willing to disclose all of the terms and conditions without any hesitation.

Step 4 – Complete Paperwork

After you have selected the best quote, your buyer and insurance company will process the documentation. Once you have completed all these, the remaining process will take a few weeks normally four to five weeks.

Documents You’ll Need to Sell Your Structured Settlement:

- Two ID proofs

- A properly filled up application form

- Your original annuity contract

- Release agreement

Step 5 – Schedule a Court hearing

If you are selling a structured settlement, it’s mandatory for you to get court approval. After completing the paperwork, your attorney will get a court date to hear your request. If the judge is satisfied with your reason to sell your annuity assets and gives you permission, your lawyer will arrange the payment for you.

Step 6: Get Approved and Receive Your Money

The insurance company that sold you the annuity product, needs to agree and approve the transaction of selling the commercial annuity. As long as you got the court approval or, the sale is legal and the buyer is reliable to do business with, the insurer wouldn’t complain and give you the approval you need.

Remember, selling your future payment for present gain is always attached to sacrificing the future for the present. Therefore, you need to think critically about whether or not you really need to sell your annuity payment.

Check out: How to buy Technology Applications in 2021